If Markets Were Efficient, Why Regulate? The 2025 SEBI (LODR) Amendment and the Limits of Efficient Capital Markets Theory

– Pragya Jha

Introduction

The central purpose of the capital market is to channel ownership rights in capital to those who value them most. For this to work, the market must set prices that tell the true story, the prices that reflect all available information. When this happens, companies can decide how much to produce or invest, and investors can choose which shares to buy or sell with confidence, because the price already captures everything that is known about the company at that moment. A market in which prices always “fully reflect” available information is called efficient.

According to the Efficient Capital Markets Theory (“ECMH”) markets naturally adjust prices in a way that reflects everything that is currently known. Whenever new information becomes available, prices change immediately to incorporate it. As a result, the current price of an asset is treated as an accurate estimate of its value at that moment. If this idea holds true, no investor can regularly make higher-than-normal profits just by relying on public information, because the price has already absorbed it. The theory assumes that information flows freely to all participants, that people make reasonable decisions based on it, and that the market reacts quickly enough to correct mistakes on its own. In this ideal setting, the market does not require outside intervention to stay fair and efficient because any mispricing or attempt to take unfair advantage disappears almost instantly. Henceforth, ECMH assumes markets are efficient in nature.

But in reality, markets don’t become efficient automatically. Information is not always complete, timely or equally accessible. Companies may choose to disclose selectively and investors may act irrationally. Prices can be distorted by insider trading, accounting manipulation, dominant shareholders or coordinated trading strategies. And that is where the need for a regulatory oversight or the hand of the law is felt. The regulations aim to create an environment in which reliable information is more likely to be produced, shared, and acted upon.

The purpose of this article is to address this gap of the ECMH that assumes markets become efficient on their own. This article proceeds in five parts. It first explains the core assumptions of the Efficient Capital Markets Hypothesis and then examines how real-world frictions undermine them. It next develops a law and economics justification for regulatory intervention, before analyzing the 2025 amendments to the Securities and Exchange Board of India (LODR) Regulations. It concludes by assessing whether these reforms move Indian capital markets closer to genuine informational efficiency.

Need For Market Regulation

The ECMH relies upon an ideal world situation where prices adjust instantly and perfectly to every piece of available information in other words it presumes a market which is efficient automatically. However, when theoretical assumptions confront real-world uncertainties, the limitations of the theory become visible. The three major assumptions upon which ECMH is based upon are; (i) everyone has equal access to information, (ii) investors are rational processors of the available information & (iii) any mispricing is self-corrected by the market itself.

The assumption of the theory is that everyone has equal access to information. In practice, markets are characterized by informational asymmetry. For instance, insider trading where people of a company such as senior executives, promoters with confidential or price sensitive information trade before the public knows the news. SEBI’s own investigation statistics show that insider trading and market manipulation cases dominate its enforcement workload. In financial year 2022-23 alone, SEBI initiated 144 investigations, of which 59% related to insider trading. Similarly, on the completion side out of 152 completed investigations that year, 49% involved insider trading cases.

Additionally, ECMH assumes that once information reaches the market, investors analyze it calmly, logically and without any bias. In such an idealized world, people behave rationally. In reality, investors just like other human beings are found to make even predictable mistakes. The Prospect Theory an important finding in Behavioral Economics showcases that people dislike losses far more than they like equivalent gains. Which means losing Rs. 1000 feels much worse than gaining Rs. 1000 feels good. This is called loss aversion which evidently shows how investors behave under uncertain market conditions. In study, the loss aversion coefficient (λ) was estimated around 2.25, meaning people feel the pain of a loss roughly 2.25 times as strongly as the pleasure of a comparable gain. Another defeating argument to the ECMH’s assumption of rational investors is the phenomenon of Herding Behaviour. People during decision making just often base their decisions not on their own information but on what they see others doing. That depicts that even if every investor has access to the same information, they may still behave irrationally simply because others are doing so.

Another point of departure from ECMH is the belief that mispricings are self-corrected by such an efficient market as presumed by the theory itself. But financial markets are social systems where strategic behavior often creates inefficiencies instead of eliminating them. High-profile cases involving index manipulation, circular trading, and coordinated derivative-cash strategies illustrate this reality. A notable recent example includes the SEBI proceeding against Jane Street, where the regulator alleged that the firm manipulated index-linked securities and earned massive profits. Such instances show that sophisticated players can actively move prices away from fundamentals and then profit from the engineered deviation.

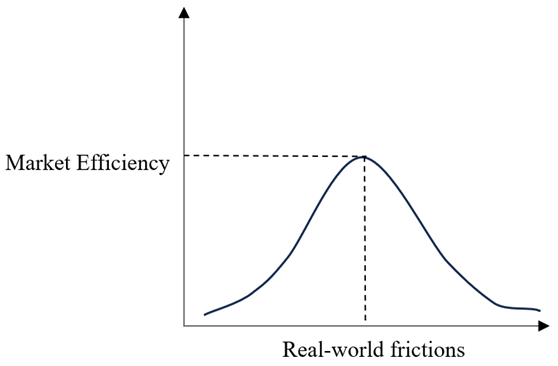

The overall analysis brings us to the conclusion that markets aren’t efficient automatically because of market uncertainties or real-world frictions as discussed till now, which weakens the presumption of ECMH. The graph above helps illustrate this point. It shows that market efficiency increases only up to a certain level of real-world frictions, marked by the dotted lines. Beyond this point, problems such as information gaps, herd behavior, and market manipulation begin to pull efficiency down, causing the curve to slope downward. This means that in real markets, efficiency does not sustain itself naturally some level of regulation is needed to maintain efficient outcomes.

A Law and Economics Perspective on the SEBI (LODR) Amendment Regulations, 2025

The SEBI (Listing Obligations and Disclosure Requirements) Amendment Regulations, 2025 reflect a deliberate regulatory attempt to correct structural inefficiencies in Indian capital markets through targeted, incremental reforms rather than a wholesale overhaul of the framework.

The amendments primarily recalibrate existing disclosure and governance norms such as:

Tighter Timelines and Expanded Scope of Material Disclosures

One of the most significant changes under the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Fourth Amendment) Regulations, 2025 is the tightening of disclosure timelines under Regulation 30 coupled with a more granular specification of what constitutes a material event. The amendments require listed entities to disclose material information arising from board decisions within 30 minutes of the conclusion of the board meeting, while other material events such as regulatory actions, litigation outcomes, defaults, restructuring decisions, and governance failures must be disclosed as soon as reasonably possible and no later than 12 hours from the occurrence of the event. This marks a clear departure from earlier, more flexible timelines that allowed informational advantages to persist for longer durations.

Delayed disclosure allows insiders and informed traders to extract informational rents, leading to unfair wealth transfers and distorted price discovery. By compressing disclosure timelines, the amendments reduce the information advantage window, thereby lowering expected gains from opportunistic trading. From an efficiency standpoint, this reduces adverse selection and improves liquidity, as uninformed investors face lower risk of trading at distorted prices. Legally, by enumerating specific events rather than relying solely on managerial discretion, SEBI reduces ambiguity and post-hoc rationalisation by firms. This shifts compliance from a subjective “judgement call” to an objective obligation, lowering enforcement costs and increasing predictability.

Mandatory Confirmation or Denial of Market Rumours

The (Fifth Amendment) Regulations, 2025 significantly strengthen the market-rumour framework by mandating that listed entities promptly confirm, deny, or clarify market rumours reported in mainstream media or digital platforms when such rumours have a material impact on the price or trading volume of the entity’s securities. For securities forming part of widely tracked indices, the amendments impose a time-bound disclosure obligation, requiring clarification within 24 hours of the rumour being reported. Importantly, the amendments treat silence or delayed responses as a compliance failure, thereby eliminating the earlier regulatory ambiguity where non-response could be justified as neutrality.

Unverified rumours create noise-driven volatility and allow speculative trading disconnected from fundamentals. Economically, this imposes negative externalities on the market by increasing volatility and undermining investor confidence. The confirmation requirement internalises this externality by placing the cost of clarification on the entity best positioned to verify the information. From a legal perspective, this amendment recognises that non-disclosure itself can be value-relevant conduct. By attaching regulatory consequences to silence, SEBI realigns incentives and discourages strategic opacity.

Expanded Coverage and Stricter Approval of Related Party Transactions

The 2025 amendments to Regulation 23 expand the scope of related party transactions by expressly covering direct and indirect transactions involving promoter group entities, relatives of promoters, and entities in which promoters or key managerial personnel exercise significant influence, even where such transactions are structured through layered or intermediary arrangements. The amendments also strengthen approval requirements by mandating prior audit committee approval for all material related party transactions, with enhanced disclosure obligations regarding the nature, purpose, and financial impact of such transactions. In certain cases, shareholder approval excluding related parties from voting has been made compulsory, thereby limiting promoter control over approval outcomes.

In promoter-dominated ownership structures, related party transactions are a principal mechanism through which controlling shareholders extract private benefits at the expense of minority shareholders. These transactions increase agency costs and distort capital allocation by diverting firm resources toward non-value-maximizing uses. By raising the procedural and disclosure costs associated with related party transactions, the 2025 amendments increase the expected cost of tunnelling behavior, making opportunistic conduct economically less attractive.

From a legal standpoint, the emphasis on ex-ante approval and independent oversight reflects an economically efficient regulatory design. Preventive governance mechanisms reduce dependence on ex post enforcement through litigation or regulatory action, which is often slow, expensive, and ineffective in markets characterised by dispersed and relatively weaker minority shareholders. By intervening at the transaction-approval stage, Regulation 23 lowers enforcement costs while improving minority shareholder protection.

Conclusion

The analysis of the ECMH in this article reveals a fundamental gap between theoretical assumptions and market realities. While ECMH is premised on the idea that markets naturally absorb all available information through rational decision-making and self-correction, the discussion demonstrates that this process is routinely disrupted by informational asymmetries, behavioral biases, and strategic conduct by powerful market participants. These frictions prevent information from being disseminated evenly or reflected instantaneously in prices, calling into question the assumption that efficiency is an automatic outcome of market functioning.

Against this backdrop, the SEBI (Listing Obligations and Disclosure Requirements) Amendment Regulations, 2025 were examined as a practical response to the limitations exposed in the theory. The tightening of disclosure timelines, the introduction of time-bound obligations to confirm or deny market rumours, and the expanded scrutiny of related party transactions directly address points where informational efficiency is most likely to break down. Rather than assuming that information will flow freely, the amendments seek to structure and accelerate its release, thereby reducing the scope for informational advantages and governance-driven distortions.

Taken together, the analysis suggests that market efficiency is not a self-sustaining condition but one that depends on institutional and legal support. Though the Efficient Capital Markets Hypothesis remains a useful benchmark, but its relevance in practice is contingent upon the regulatory frameworks that enable information to be timely, accurate, and accessible.

The author is student of Gujarat National Law University, Gandhinagar.